RETECHNOLOGY PREMIUM MARKETPLACE RELATED PRODUCTS | WEBINARS | SPECIAL OFFERS

You are viewing our site as a Broker, Switch Your View:

Agent | Broker Reset Filters to Default Back to ListHUD Announces New FHA Loan Limits for 2018

December 19 2017

Loan limits to increase in more than 3,000 counties

WASHINGTON - The Federal Housing Administration (FHA) today announced the agency's new schedule of loan limits for 2018, with most areas in the country to experience an increase in loan limits in the coming year. These loan limits are effective for FHA case numbers assigned on or after January 1, 2018.

- Read FHA's Mortgagee Letter on 2018 Forward Mortgage Limits

- Read FHA's Mortgagee Letter on 2018 Home Equity Conversion Mortgage (HECM) Limits

FHA is required by the National Housing Act, as amended by the Housing and Economic Recovery Act of 2008 (HERA), to set Single Family forward loan limits at 115 percent of median house prices, subject to a floor and a ceiling on the limits. FHA calculates forward mortgage limits by Metropolitan Statistical Area and county.

In high-cost areas of the country, FHA's loan limit ceiling will increase to $679,650 from $636,150. FHA will also increase its floor to $294,515 from $275,665. Additionally, the National Mortgage Limit for FHA-insured Home Equity Conversion Mortgages (HECMs), or reverse mortgages, will increase to $679,650 from $636,150. FHA's current regulations implementing the National Housing Act's HECM limits do not allow loan limits for reverse mortgages to vary by MSA or county; instead, the single limit applies to all mortgages regardless of where the property is located.

Due to robust increases in median housing prices and required changes to FHA's floor and ceiling limits, which are tied to the Federal Housing Finance Agency (FHFA)'s increase in the conventional mortgage loan limit for 2018, the maximum loan limits for FHA forward mortgages will rise in 3,011 counties. In 223 counties, FHA's loan limits will remain unchanged. By statute, the median home price for an MSA is based on the county within the MSA having the highest median price. It has been HUD's long-standing practice to utilize the highest median price point for any year since the enactment of HERA.

The National Housing Act, as amended by HERA, requires FHA to establish its floor and ceiling loan limits based on the loan limit set by FHFA for conventional mortgages owned or guaranteed by Fannie Mae and Freddie Mac. Today, FHA's minimum national loan limit, or floor, is set at 65 percent of the national conforming loan limit of $453,100. This floor applies to those areas where 115 percent of the median home price is less than the floor limit. Any areas where the loan limit exceeds this ‘floor' is considered a high-cost area, and HERA requires FHA to set its maximum loan limit ‘ceiling' for high-cost areas at 150 percent of the national conforming limit.

Prior to the passage of HERA, the National Housing Act (NHA) provided that the FHA mortgage limit for any given area be set at 95 percent of the median one-family house price in that area, as determined by HUD. However, the NHA further stated the FHA mortgage limit in any given area cannot exceed 87 percent of the Freddie Mac loan limit (305(a)(2) of the Federal Home Loan Mortgage Corporation Act (12 U.S.C. 1454(a)(2)), nor be less than 48 percent of that limit. Since the enactment of HERA and The Economic Stimulus Act of 2008, which temporarily raised FHA limits even further, FHA's loan limits have been more closely tied to, and at times in excess of, those for GSE-eligible loans.

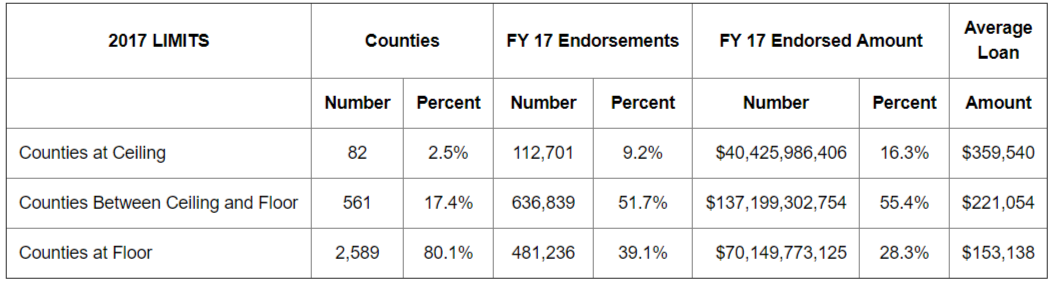

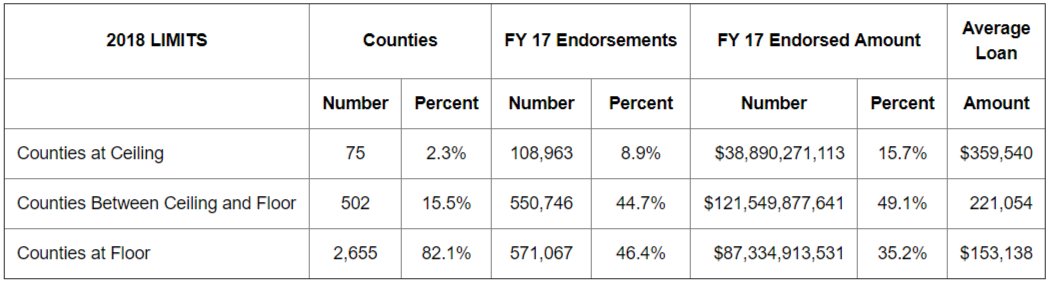

Based upon the volume of FHA endorsements in FY 2017, the following charts represent the number and share of counties where FHA loan limits are at the ceiling, floor and somewhere in between.

To find a complete list of FHA loan limits, areas at the FHA ceiling, areas between the floor and the ceiling, as well as a list of areas with loan limit increases, visit FHA's Loan Limits Page.