RETECHNOLOGY PREMIUM MARKETPLACE RELATED PRODUCTS | WEBINARS | SPECIAL OFFERS

You are viewing our site as an Agent, Switch Your View:

Agent | Broker Reset Filters to Default Back to ListIf Interest Rates Rise, How Can It Be the Best Time to Buy?

July 19 2017

The Federal Reserve has increased interest rates twice so far this year and, according to a survey by the Wall Street Journal, will possibly do so one more time this year. With conventional wisdom believing that interest rates could head higher, how can it be the best time to buy a home?

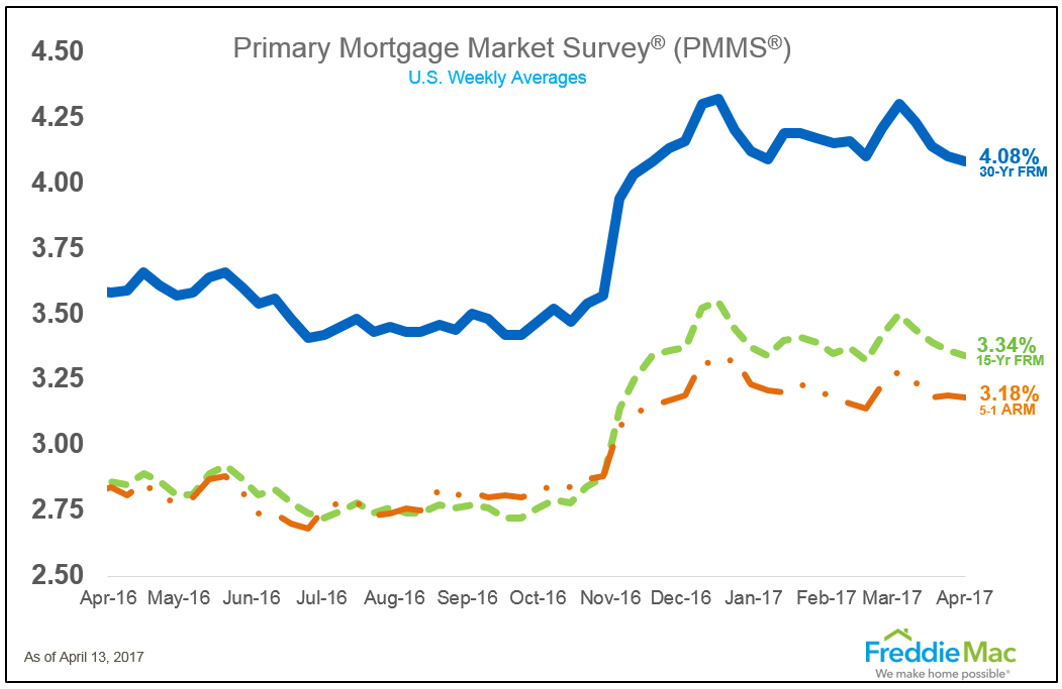

Impact on mortgage rates

The first thing to look at is what has happened to mortgage interest rates since the last time the Fed increased the Federal Fund Rate in March, from 0.75 to 1.00 percent. Mortgage interest rates have actually dropped, according to the Freddie Mac Primary Mortgage Market Survey.

The Fed interest rate hike was announced on March 15. On March 16, Freddie Mac announced the 30-Year Fixed Rate Mortgage was 4.30 percent and the 15-Year Fixed Rate Mortgage was 3.50 percent. On March 23, the rate dropped to 4.23 percent for the 30-Year and 3.44 percent for the 15-Year. The next week, on April 6, the rates dropped again to 4.10 percent and 3.36 percent for the 30- and 15-year mortgages respectively, and they have continued on this trend.

The Federal Reserve does not control mortgage rates. They control the Federal Funds Rate and that is the interest rate that banks pay to lend money to each other, not to you and me. There is no direct cause and effect to what the Fed does with 30- and 15-year fixed mortgage rates, except to their tapering of their balance sheet repurchases. And on this front, we do not believe they will do anything to disrupt the housing market. Rates have gone relatively "sideways" since January, and that makes the affordability of rates even more important to consider.

What historically low means: better affordability

When you hear the phrase "mortgage interest rates remain historically low," the problem is that 30-year fixed rate mortgage interest rates have been below 5 percent for so long, we forget that people were buying homes with 13 percent interest rates in the 1980s; 10 percent interest rates in the 1990s and 8 percent interest rates in the 2000s.

When we compare interest rates today with interest rates and mortgage payments historically, we forget to consider the impact of inflation. As we have shared before, when you look at mortgage payments today, and you make the adjustments for inflation, we are paying 20 percent less than we did for a mortgage in 1989. Compared to when housing prices peaked in the summer of 2007, we are paying 35 percent less in mortgage payments today than we did then.

Trying to catch a falling knife

There's a phrase in the financial services business that describe the behavior of customers who try to wait for interest rates to drop to their lowest levels to lock in the lowest rate possible: "It's like trying to catch a falling knife: it's nearly impossible to do without getting hurt." More importantly, it really is unnecessary when you consider what happens when mortgage rates rise – they can jump, and jump quickly. The fact is that no one can predict when mortgage rates rise and the best advice to any customer is if you like the interest rate, lock it in and know you will have obtained one of the lowest historical rates in the history of the world.

Interest rates move up and down within a range, or are "range-bound," and most economists predict, barring an unplanned economic disaster, that interest rates are likely to stay within a range that fall below the 5 percent threshold, but if you are waiting to buy, both real estate agents and mortgage advisors will tell you from experience: don't wait if you can afford the purchase and it serves your family's concerns.

When mortgage rates do rise, they do tend to jump up to a new range, as they did after the election in November. When you think about the impact higher mortgage rates can have on your purchasing decision, it can be a bigger motivator to act now versus waiting.

Buying a $500,000 home with a 20 percent down payment and with a mortgage at 6 percent versus a mortgage at 4 percent means paying 61 percent more in total interest payments. So when you see interest rates still remaining under 5 percent today, even with interest rates rising, relative to historical rates, buying now is clearly the best time to buy.

Susan McHan, as President of Distributed Retail Mortgage Division at Opes Advisors, a Division of Flagstar Bank, is bringing to fruition her lifelong journey of helping people make the most effective financial decisions to support their current lifestyle and prepare for a satisfying future.

Susan McHan, as President of Distributed Retail Mortgage Division at Opes Advisors, a Division of Flagstar Bank, is bringing to fruition her lifelong journey of helping people make the most effective financial decisions to support their current lifestyle and prepare for a satisfying future.